The euro navigated a tricky week, ultimately on track to end lower the week down. A surprise windfall tax, to be levied on Italian banks, was announced on Tuesday, sending the pair sharply lower. Prices recovered the following day upon reassurance from the Italian president that the tax would amount to no more than 0.1% of total bank assets. US inflation then edged higher, something the market appeared content with but after a volatile daily move had the pair near flat on the day.

In the week to come there is a notable drop-off in terms of high impact risk events with EU and German ZEW economic sentiment the only standouts. Final inflation data for July and the second estimate of Q2 GDP is unlikely to move the needle much unless the data differs significantly from prior readings.

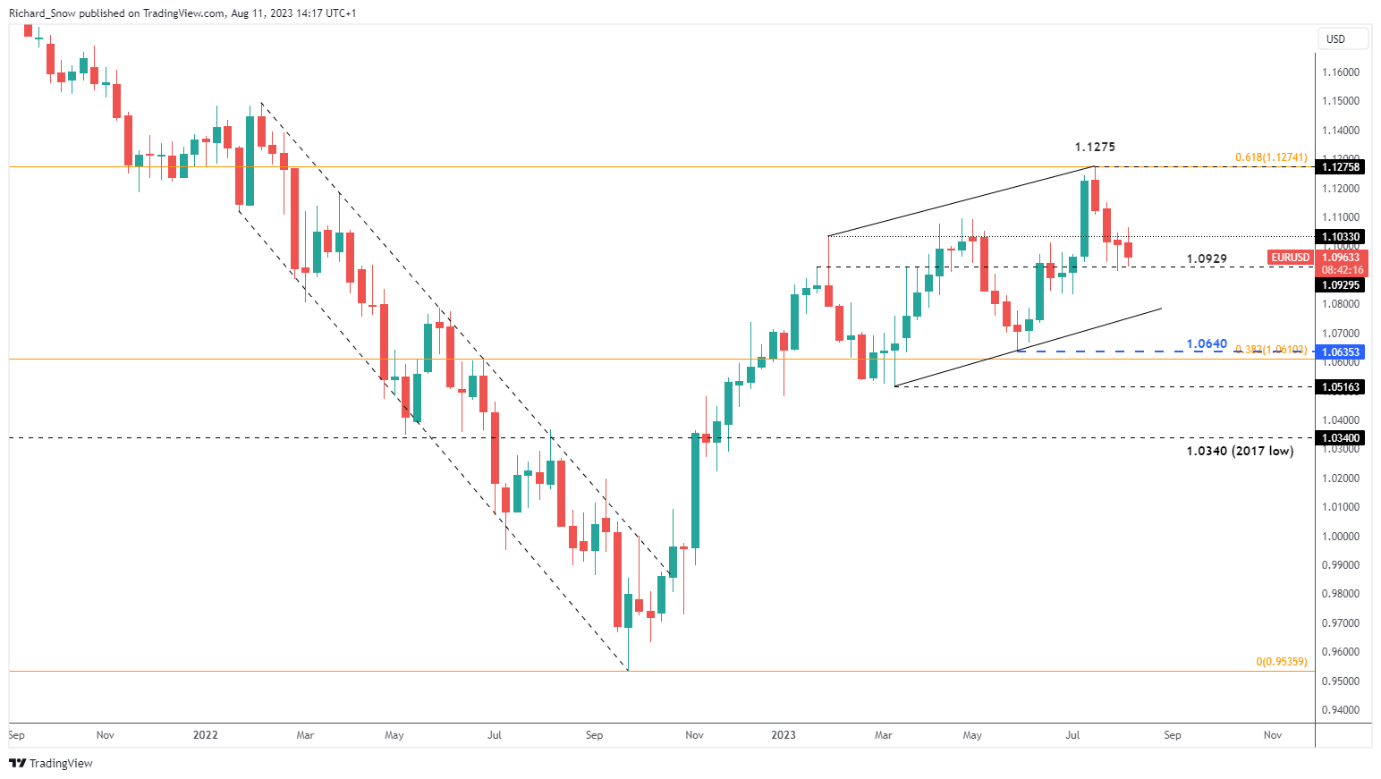

The daily chart opens up the possibility for the pair to trade between 1.1012 and 1.0910 in the week to come. With inflation in the US and Europe broadly moving in the right direction and both regions’ central banks at or very close to reaching terminal rates, there are fewer obvious drivers for either currency.

EUR/USD Daily Chart

The weekly chart shows the longer-term uptrend which has developed in a rather choppy fashion, now heading lower but stalling at the 1.0930 level. In the event the bearish directional move extends, 1.0833 becomes the next level of interest (a level that corresponds to the weekly lows at the end of June and early July).

Markets have a consensus view that the ECB will pause rate hikes in September but still price in the possibility of another 25-bps hike before the end of the year. Economists polled by Reuters revealed a slight majority of economists (53%) agree with that view. Stubborn core inflation in the EU for July complicates the situation but given the deteriorating economic data (German and EU manufacturing PMI and a growth slowdown, despite a slight improvement in Q2 GDP) weighs on the ECB’s hawkish resolve.

Market Implied Rate Expectations

{kind=link}